<a href="http://www.shutterstock.com/pic.mhtml?id=103079882">Brian A Jackson</a>/Flickr

Last month I wrote a post showing that retiree income had risen 75 percent between 1971 and 2011. Conversely, the median income of middle-aged workers has grown a bit less than 8 percent. This is one reason that I’m not super-excited about increasing taxes on the working-age population in order to prevent even the tiniest reduction in the future growth rate of Social Security benefits.

As you can imagine, I got some pushback on this. The strongest criticism was pretty simple: In the private sector, old-style defined-benefit pensions began fading away three decades ago, replaced by less generous 401(k)-style plans that don’t provide the same level of retirement security. But that’s not going to show up as a noticeable fall in retiree income until workers who turned 30 in the mid-’80s start to turn 65. Instead of looking at historical data, then, I need to look ahead to retiree income in 2020 and beyond. That turned out to be harder than I thought it would be, but I’ve found a few useful comparisons. Here they are.

First off: There’s no question that defined-benefit pensions have all but disappeared in the private sector. The Employee Benefit Research Institute (EBRI) tracks this stuff, and their findings are stark. In the private sector, DB plans used to cover 38 percent of all workers but now cover only about 15 percent. At the same time, the number of workers with 401(k)-style defined-contribution plans has skyrocketed from 17 percent to 43 percent. This is a sea change in worker pensions.

By itself, though, it doesn’t tell us much. What we want to know is how much the old DB plans paid out on average compared to newer 401(k) plans. In fact, what we really want to know is total retiree income from all sources, projected into the future. This is a little tricky, so bear with me.

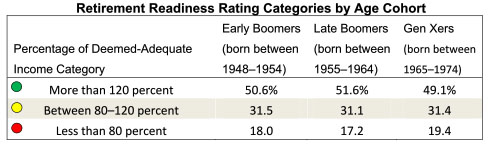

The most common way of forecasting retirement income is via an index that tracks something called “retirement readiness.” The usual takeaway from these kinds of metrics is that fewer and fewer workers are likely to have enough income to replicate their pre-retirement lifestyle. But again, this doesn’t tell us very much. For one thing, these indexes are usually a little opaque. For another, they don’t tell us how far people are falling short. Are there a lot of people who used to be 1 percent above the readiness cutoff and are now 1 percent below, or is it more serious?

A couple of months ago EBRI came to the rescue with something a little more useful. For various age groups, they showed how many workers are close to retirement readiness vs. well below retirement readiness. Here’s the table:

This suggests that there’s not actually a lot of change projected for the future. Gen Xers, who will begin retiring in 2030, appear to be in about the same overall shape as Boomers.

But those three categories still have a fair amount of play in them. After all, there’s a big difference between being at 119 percent of readiness vs. 81 percent. What I’d really like to see are projections of retirement income going into the future. EBRI’s Jack VanDerhei suggested I might find this in the MINT simulations from the Social Security Administration, and Howard Iams of the SSA was kind enough to send along the relevant report. Its conclusion was two-sided:

Future retirees are projected to have higher incomes and lower poverty rates, and so their prospects look better than current retirees in absolute terms. However, future retirees are also projected to have lower replacement rates, and so their prospects are actually worse than current retirees in relative terms.

“Replacement rate” is the percentage of your pre-retirement income that you get when you retire. The typical Depression-era worker had a replacement rate of 95 percent, while the typical Gen Xer is expected to have a replacement rate of only 84 percent. So in that sense, today’s workers really are worse off than previous generations.

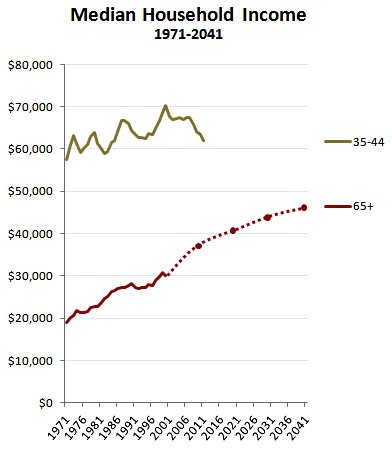

But there’s more to this. Gen Xers might have lower replacement rates, but the incomes they’re replacing are much higher. This means that in dollar terms (adjusted for inflation), their retirement incomes are considerably larger than previous generations. To show what this looks like, I’ve very roughly combined historical income data with projected income data (from Table 3 in the MINT report) to produce the chart on the right. It’s the same chart from my post last month, but with MINT’s forecasts added. The top line shows the fairly stagnant incomes of middle-aged workers. The bottom line shows the steady increase in income among retirees, which has risen from $20,000 in 1971 to about $38,000 today, and is projected to rise to $46,000 by  2041. This is income from all sources: defined-benefit plans, 401(k) plans, Social Security, earnings, and investments.

2041. This is income from all sources: defined-benefit plans, 401(k) plans, Social Security, earnings, and investments.

If these projections are right, future retirees are in pretty good shape in pure dollar terms. At the same time, their retirement incomes are going to be a lower percentage of their pre-retirement income than in previous generations. You can paint either a grim picture or a happy one if you cherry pick only one of these findings.

For myself, I keep looking at that middle-aged income line. Unless things change pretty dramatically, it looks to me as if working-age incomes are going to continue being pretty flat. I’m not happy about this state of affairs, but there’s not much reason to think it’s going to change. At the same time, retiree incomes are continuing to rise, and this puts me right back where I started: Because current workers are doing relatively worse than retirees, I’m not too excited about increasing their taxes in order to prevent even a tiny slowdown in the growth of future Social Security benefits. This is especially true for higher-income retirees.

So what choices does that leave us? One option is to make Social Security solvent solely by raising taxes on the rich. But that would require a whopping big tax increase. A second option is to do nothing and just see how things play out. Five years ago I would have been okay with that, but recent trust fund projections make me nervous about this. A third option is to raise taxes on middle-income workers, and I’ve already explained why I’m not too excited about that prospect. Given all this, and given the relative prosperity of retirees above the median, my preference for addressing the solvency of Social Security is to (a) raise the payroll tax income cap somewhat but not raise rates, (b) keep benefits the same or higher at low income levels, and (c) modestly cut the growth rate of benefits at income levels above the median.

NOTE: The lines in the chart above are necessarily rough because the historical data comes from a different source than the projections. This makes it hard to do a true apples-to-apples comparison. If I come across something more rigorous, I’ll let you know.

NOTE #2: This post is about long-term trends in retirement incomes. It doesn’t address the problems of sixtysomethings who are very near to retirement right now, some of whom have suffered reversals in their retirement accounts due to the Great Recession. I don’t have any data at hand about how big a problem that is. It’s a post for another time.