Getty Images

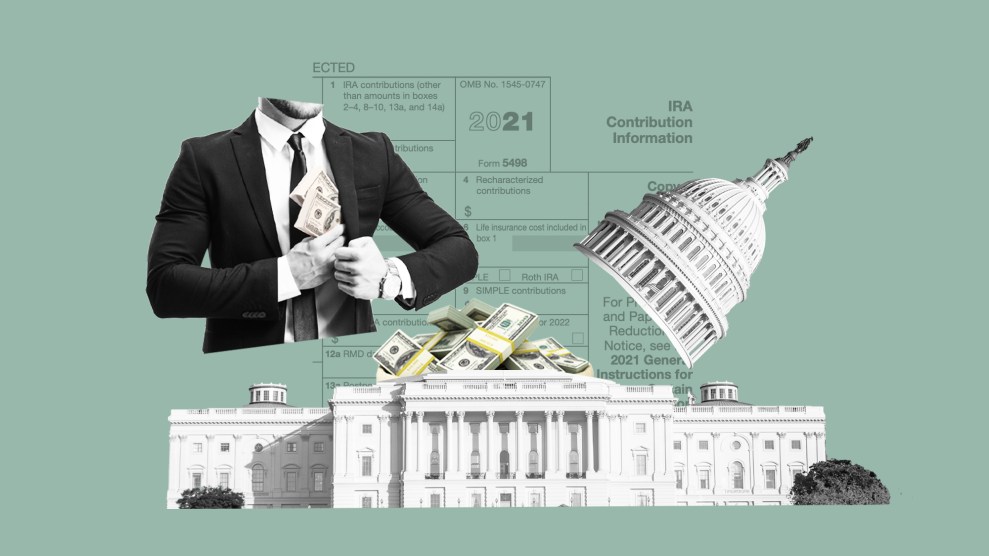

In 2016, when Donald Trump was campaigning for president, he got a ton of mileage out of lamenting, to all who would listen, that “the system is rigged” against ordinary Americans. Which it is. But Trump usually neglected to note that the “system”—of taxation, for one—is rigged by financial professionals hired by rich people like him, and their companies, to make the whole lot of them richer.

The New York Times‘ Jesse Drucker and Danny Hakim reported Sunday on one slice of this game: the revolving door between massive accounting firms like KPMG, EY, PwC, Deloitte, and RSM and the Treasury Department, where tax guidelines enacted by Congress are put into practice:

From their government posts, many of the industry veterans approved loopholes long exploited by their former firms, gave tax breaks to former clients and rolled back efforts to rein in tax shelters—with enormous impact.

According to the report, these private-sector professionals, after a relatively short stint at Treasury pushing tax workarounds desired by their clients, or helping to kill or water down proposals that might cost clients money, are then welcomed back at their firms, which often reward them with lucrative raises and promotions. As Drucker and Hakim noted…

In the last four presidential administrations, there were at least 35 instances of round trips from big accounting firms through Treasury’s tax policy office, along with the Internal Revenue Service and the Congressional Joint Committee on Taxation, and back to the same firm, according to public records and interviews with government and industry officials.

In at least 16 of those cases, the officials were promoted to partner when they rejoined their old accounting firms. The firms often double the pay of employees upon their return from their government sojourns. Some partners end up earning more than $1 million a year.

It’s solid reporting, and for those of us who keep a close eye on the tax shenanigans of the ultra-rich, not surprising in the least. For while ordinary Americans may deride our most ludicrously wealthy citizens for rigging the system, the dirty work is performed largely by professional and financial firms—and the lobbyists they hire to ensure their customers can pay as little tax as possible within the letter, if not the spirit, of the law.

“It’s the suppliers of tax-avoidance services,” said University of California-Berkeley economist Gabriel Zucman during an interview for my recent book on wealth in America. “That includes part of the financial industry, wealth managers, and some of the law firms. That’s what’s always pushing tax avoidance and tax evasion: people who create products, who market them with rich people and make it possible for them to dodge taxes.”

The revolving door goes well beyond the accounting industry, of course. The Treasury Department is often full of people with close ties to Wall Street firms, and Goldman Sachs in particular—Hank Paulsen and Steve Mnuchin come to mind. As I wrote in an earlier piece, when the Obama administration sought to regulate financial partnerships like private equity firms and hedge funds, whose opaque, leveraged transactions can destabilize the markets, a group called the Private Investor Coalition jumped into action.

The coalition represents the interests of family offices—private companies that the nation’s richest families launch to manage their affairs. These families wanted to be exempt from regulation, and their effort succeeded, thanks in part to Jake Sehar, a lobbyist hired on the coalition’s behalf, who also happened to be a former longtime aide to Sen. Joe Biden, who was then vice president.

The revolving door ties described by the Times, and lobbying by other former government officials, will make a big difference in the success or failure of the Biden administration’s efforts to level the economic playing field, and how any such changes are implemented.

For years, activists have been highlighting huge gaps in wealth and opportunity based on a person’s ethnicity and family circumstances. The proliferation of multibillionaires—indeed, their very existence—demonstrated for some critics the moral depravity not just of shareholder-focused capitalism, but of tax policies that enable a tiny number of Americans to amass and protect epic fortunes even as the majority stagnates.

The Biden administration came into power, mid-pandemic, with the lofty goal of trying to curb the worst of the wealth disparities, and it made modest progress via the last COVID relief bill. But with a razor thin Senate margin, a few moderate spoilers, and a host of corporate lobbyists and insiders representing the interests of wealthy donors of both parties, Biden’s ambitions are running into a wall of political reality.

The Dems, for instance, want to raise the top marginal income tax rate from 37 percent back to its pre-Trump level of 39.6 percent. That will probably fly, if only because rich folks know that something has to give.

Top marginal rates only apply to the uppermost portions of a high earner’s income (after deductions). For 2021, if you’re married and filing a joint return, you’ll pay less than 24 percent on earnings up to $329,850, no more than 35 percent on additional earnings up to $628,300, and 37 percent thereafter. The Dems’ proposal adds another category, so if you earn millions annually, that change will cost an extra $26,000 per million. It would also tweak the brackets so the above-mentioned taxpayer would pay the maximum rate on any portion of their gross income exceeding $450,000.

But many of America’s richest already sidestep income taxes by avoiding income altogether. With vast private and public investment holdings as collateral, it’s easy for 0.01 percenters and up to secure low-interest loans to bankroll their lavish lifestyles. When the loans come due, they can take out new ones—and sometimes even claim tax deductions on the interest. Billionaires like Jeff Bezos, Warren Buffett, Bill Gates, Elon Musk, George Soros, Mark Zuckerberg, and more, as ProPublica recently revealed, pay exceedingly little income tax relative to their annual wealth gains—which have accelerated immensely since the start of the pandemic.

The Dems also want an additional 3 percent surcharge on incomes exceeding $5 million. Together with the boost in the top marginal rates, that will cost a taxpayer with earnings of $10 million more than $500,000 annually. That might happen, but I consider it a long shot.

Where congressional Democrats have really caved is on capital gains. They propose to raise the top tax rate on capital gains (and stock dividends) from 20 percent to 25 percent—a spineless compromise, given that Biden wanted to charge 39.6 percent, the same maximum rate he proposed for ordinary wage income.

Capital gains are the difference between the cost of an asset (like stock) and the amount you get when you sell it. Short term cap gains (for assets sold within a year of their purchase) are already taxed at the same rate as wages. Under current law, a married taxpayer filing jointly who reaps up to $501,600 in long-term capital gains (on the sale of investments held at least a year) pays only 15 percent. Any profits in excess of that amount are taxed at 20 percent.

But most Americans have few, if any, invested assets, while the richest rely primarily on such assets. Policies that favor investment earnings over wage earnings are therefore a key driver of wealth inequality. Even if the proposal flies—and corporate lobbyists are out in force on this one—it won’t move the needle of inequality that much.

The maximum corporate income tax rate, which the Republicans unilaterally slashed in 2017 from 35 percent to 21 percent, would only bump up to 26.5 percent under the Democratic proposal—down from Biden’s goal of 28 percent. It seems the lobbyists have already won that round.

Another point of contention are inheritances, on which America’s richest families pay an effective tax rate of only 2 percent. The Dems propose to cut the gift/estate tax exemption from $11.7 million to about $6 million. The exemption is the total amount that a person, in life or via their estate after death, can dole out to heirs and others tax-free. (Spouses are exempt.) The 2017 Republican tax cuts temporarily doubled the exemption, which is set to revert to about $6 million after 2025 anyway, so this proposal would simply accelerate the schedule. For now, a married couple can leave twice the individual exemption—or $23.4 million—to their princelings without paying a dime in tax.

Biden also wants to reveal the lucrative “step-up in basis” rule. Say I buy a million shares of stock at a dollar a share, and sell it 30 years later for $100 a share. I have to pay capital gains tax on my $99 million in profits. But if I die and leave the stock to my kids, the “basis” price resets to the stock’s current value, so now my heirs can sell the shares and pay nothing. Policymakers could repeal this rule and leave exceptions for small inheritances and family farms and small business, or set the exemption high. But rich families from both parties—and the wealth management industry—won’t give this perk up willingly. The House version of the reconciliation legislation doesn’t include such a proposal, so don’t hold your breath.

You can also expect the wealth industry to fight like hell to kill a Democratic attempt to rein in “grantor” trusts. In 1990, lawmakers tweaked the tax code to curb the abuse of another kind of trust that lawyers were using to reduce clients’ estate taxes a few percent. They accidentally enabled something way worse—a “grantor retained annuity trust.” The most common form is known as a Walton GRAT. Named after Audrey Walton, a member of the Walmart clan, it allows families, in some cases, to bypass gift and estate taxes almost entirely.

Sheldon Adelson reportedly used Walton GRATs to transfer almost $8 billion to his heirs tax-free, avoiding more than $2 billion in gift taxes. Marc Zuckerberg, Sheryl Sandberg, and many others have used similar trusts.

GRATs “are perhaps the most widely used advanced estate planning technique,” the law firm Shiff Hardin noted in a recent post meant for potential clients. “If the plan put forth recently by the House Ways and Means Committee “is codified, it appears GRATs will no longer be beneficial.” Eliminating GRATs and related trusts would place new limits on the ability of America’s dynasties to pass huge fortunes to their heirs free, and those families will fight hard to kill the provision.

House Ways and Means also wants to cap contributions to tax-advantaged retirement plans once a person’s combined account balances exceed $10 million. This limitation, as I explain in another piece, would help counter the fact that the hundreds of billions of dollars the federal government spends each year to subsidize retirement savings flow overwhelmingly to America’s most affluent. Will that proposal survive? It’s very hard to predict.

In literally every area of tax policy, one finds well-heeled firms and industry insiders working to secure legislation in their clients’ financial interests—and their own. Most wealth managers, for instance, charge clients based on the amount of the person’s money under management. For every dollar a private bank saves a client in taxes, it earns an extra penny or two a year, which adds up when you’re talking about tens of millions or hundreds of millions of dollars.

As Chuck Collins, whose latest book, The Wealth Hoarders, examines how financial professionals are driving economic inequality here and abroad, told me recently, “The wealth defense industry—the lawyers, accountants, and wealth managers to the super-rich…have fracked every corner of the tax code.”

They most certainly have.